Machine Learning¶

causalimpact: Find Causal Relation of an Event and a Variable in Python¶

!pip install pycausalimpact

When working with time series data, you might want to determine whether an event has an impact on some response variable or not. For example, if your company creates an advertisement, you might want to track whether the advertisement results in an increase in sales or not.

That is when causalimpact comes in handy. causalimpact analyses the differences between expected and observed time series data. With causalimpact, you can infer the expected effect of an intervention in 3 lines of code.

import numpy as np

import pandas as pd

from statsmodels.tsa.arima_process import ArmaProcess

import causalimpact

from causalimpact import CausalImpact

# Generate random sample

np.random.seed(0)

ar = np.r_[1, 0.9]

ma = np.array([1])

arma_process = ArmaProcess(ar, ma)

X = 50 + arma_process.generate_sample(nsample=1000)

y = 1.6 * X + np.random.normal(size=1000)

# There is a change starting from index 800

y[800:] += 10

data = pd.DataFrame({"y": y, "X": X}, columns=["y", "X"])

pre_period = [0, 799]

post_period = [800, 999]

ci = CausalImpact(data, pre_period, post_period)

print(ci.summary())

print(ci.summary(output="report"))

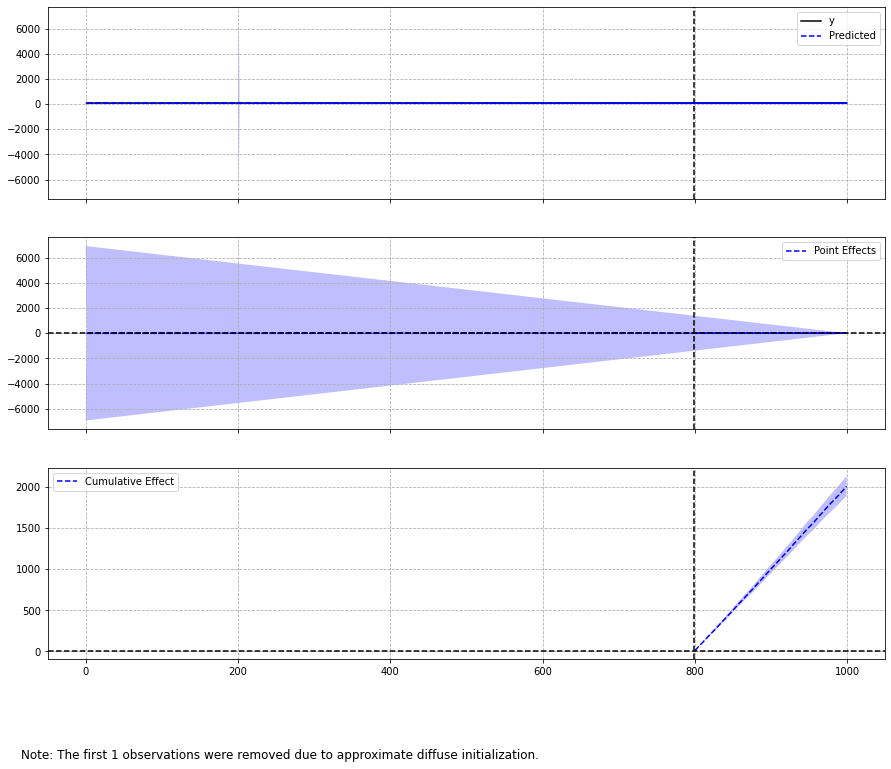

ci.plot()

Posterior Inference {Causal Impact}

Average Cumulative

Actual 90.03 18006.16

Prediction (s.d.) 79.97 (0.3) 15994.43 (60.49)

95% CI [79.39, 80.58] [15878.12, 16115.23]

Absolute effect (s.d.) 10.06 (0.3) 2011.72 (60.49)

95% CI [9.45, 10.64] [1890.93, 2128.03]

Relative effect (s.d.) 12.58% (0.38%) 12.58% (0.38%)

95% CI [11.82%, 13.3%] [11.82%, 13.3%]

Posterior tail-area probability p: 0.0

Posterior prob. of a causal effect: 100.0%

For more details run the command: print(impact.summary('report'))

Analysis report {CausalImpact}

During the post-intervention period, the response variable had

an average value of approx. 90.03. By contrast, in the absence of an

intervention, we would have expected an average response of 79.97.

The 95% interval of this counterfactual prediction is [79.39, 80.58].

Subtracting this prediction from the observed response yields

an estimate of the causal effect the intervention had on the

response variable. This effect is 10.06 with a 95% interval of

[9.45, 10.64]. For a discussion of the significance of this effect,

see below.

Summing up the individual data points during the post-intervention

period (which can only sometimes be meaningfully interpreted), the

response variable had an overall value of 18006.16.

By contrast, had the intervention not taken place, we would have expected

a sum of 15994.43. The 95% interval of this prediction is [15878.12, 16115.23].

The above results are given in terms of absolute numbers. In relative

terms, the response variable showed an increase of +12.58%. The 95%

interval of this percentage is [11.82%, 13.3%].

This means that the positive effect observed during the intervention

period is statistically significant and unlikely to be due to random

fluctuations. It should be noted, however, that the question of whether

this increase also bears substantive significance can only be answered

by comparing the absolute effect (10.06) to the original goal

of the underlying intervention.

The probability of obtaining this effect by chance is very small

(Bayesian one-sided tail-area probability p = 0.0).

This means the causal effect can be considered statistically

significant.

Pipeline + GridSearchCV: Prevent Data Leakage when Scaling the Data¶

Scaling the data before using GridSearchCV can lead to data leakage since the scaling tells some information about the entire data. To prevent this, assemble both the scaler and machine learning models in a pipeline then use it as the estimator for GridSearchCV. Above is an example.

The estimator is now the entire pipeline instead of just the machine learning model.

from sklearn.model_selection import train_test_split, GridSearchCV

from sklearn.preprocessing import StandardScaler

from sklearn.pipeline import make_pipeline

from sklearn.svm import SVC

from sklearn.datasets import load_iris

# load data

df = load_iris()

X = df.data

y = df.target

# split data into train and test

X_train, X_test, y_train, y_test = train_test_split(X, y, random_state=0)

# Create a pipeline variable

make_pipe = make_pipeline(StandardScaler(), SVC())

# Defining parameters grid

grid_params = {"svc__C": [0.1, 1, 10, 100, 1000], "svc__gamma": [0.1, 1, 10, 100]}

# hypertuning

grid = GridSearchCV(make_pipe, grid_params, cv=5)

grid.fit(X_train, y_train)

# predict

y_pred = grid.predict(X_test)

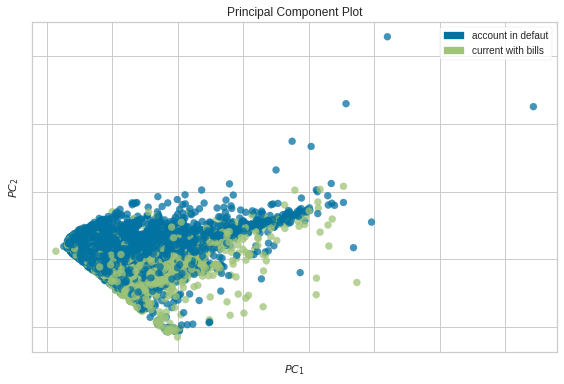

Decompose high dimensional data into two or three dimensions¶

!pip install yellowbrick

If you want to decompose high dimensional data into two or three dimensions to visualize it, what should you do? A common technique is PCA. Even though PCA is useful, I always find it complicated to create a PCA plot until I found Yellowbrick.

I really recommend using this tool if you want to visualize PCA in a few lines of code

from yellowbrick.datasets import load_credit

from yellowbrick.features import PCA

X, y = load_credit()

classes = ["account in defaut", "current with bills"]

visualizer = PCA(scale=True, classes=classes)

visualizer.fit_transform(X, y)

visualizer.show()

<AxesSubplot:title={'center':'Principal Component Plot'}, xlabel='$PC_1$', ylabel='$PC_2$'>

squared=False: Get RMSE from Sklearn’s mean_squared_error method¶

If you want to get the root mean squared error using sklearn, pass squared=False to sklearn’s mean_squared_error method.

from sklearn.metrics import mean_squared_error

y_actual = [1, 2, 3]

y_predicted = [1.5, 2.5, 3.5]

rmse = mean_squared_error(y_actual, y_predicted, squared=False)

rmse

0.5